From 6 April 2013, the UK introduced a new Statutory Residence Trust (SRT) for tax purposes. Previously, there had not been a set of coherent rules, just a mix of Case Law and Extra Statutory Concessions. The old rules led to uncertainty and recent cases demonstrated that reliance could not be placed on published HMRC guidance in this area.

However, the new rules open the possibility that

non-residents could now inadvertently trigger UK tax liability whereas under the old “rules” this would not have been the case.

If you have recently become an expatriate and/or make regular trips back to the UK, you should be aware of the rules so as not to inadvertently miss-file your Tax return

and incurring a liability.

· The SRT consists of two levels of test;

1. The “automatic tests” and

2. The “sufficient ties tests”

To apply the rules, each tax year is considered separately and the above tests are considered in sequence. Once an automatic test is “passed” no further tests are considered. The sufficient ties tests make a distinction between “arrivers” (people not resident for all of the previous tax years) and “leavers” (people who were resident for one or more of the previous three tax years).

1. The Automatic Tests

These tests are different and seek to establish immediately if you are automatically resident or non-resident. In the event of a conflict the non-residence tests take precedence.

2. The Sufficient Ties Tests

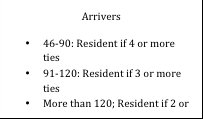

Between the above fixed points, there is a sliding day count for “arrivers” and “leavers” based on the number of ties they have to the UK. Ties are split into the following 5 categories, each with their own definitions:

– The Family Tie

– The Accommodation Tie

– The Work Tie

– The 90 Day Tie

– The Country Tie

Below sets out on a sliding scale when an individuals will be

resident based on the number of UK days and number of ties they have.

If you believe you may be in danger of having acquired UK tax residence or require further information contact Dino Zavagno at Gladstone Morgan or one of our consultants for advice in this area.

Disclaimer: All content provided on this page are for informational purposes only. Gladstone Morgan Limited makes no representations as to the accuracy or completeness of any information on this page or found by following any link on this page. Gladstone Morgan Limited will not be liable for any errors or omissions in this information nor for the availability of this information. Gladstone Morgan Limited will not be liable for any losses, injuries, or damages from the display or use of this information. This policy is subject to change at any time.

It should be noted the services available from Gladstone Morgan Limited will vary from country to country. Nothing in the comments above should be taken as offering investment advice or making an offer of any kind with regard to financial products or services. It is therefore important to reinforce that all comments above are designed to be general in nature and should not be relied upon for considering investment decisions without talking to licensed advisers in the country you reside or where your assets may located.Gladstone Morgan Ltd is not SFC authorized. Gladstone Morgan Ltd in Hong Kong is licensed with the Hong Kong Confederation of Insurance Brokers.